The Eastern Europe & Central Asia region accounted for the largest proportion of new commitments, followed by Sub-Saharan Africa and the Middle East & North Africa. A railway project in Kazakhstan was the most significant of these new commitments.

SERV issued new insurance policies worth CHF 2.641 billion for Swiss exporters in the 2023 financial year. The successful acquisition of new customers could not compensate for the decline in applications.

At CHF 2.641 billion, new commitment was lower than in the previous year (CHF 3.296 billion). The Eastern Europe & Central Asia region accounted for the largest proportion, followed by Sub-Saharan Africa and the Middle East & North Africa. SERV’s largest new commitment was for a railway project in Kazakhstan. Other countries with new commitment of more than CHF 100 million were Türkiye, Bangladesh, Benin (see sustainability case study), Egypt, Senegal, China, Iraq and the UK.

As usual, the figures for new commitments were heavily influenced by individual large projects. In the year under review, SERV insured various infrastructure projects in the railway and energy sectors. In the important textile sector, SERV again supported a number of export transactions in Benin, Egypt, Türkiye and Uzbekistan. SERV frequently supports the financing of major projects with buyer credit insurance.

Insurance policies for large projects in Russia and Brazil were terminated prematurely. As a result, premiums totalling approximately CHF 45 million were refunded. This meant that premium income for the year was lower than would have been expected in view of the newly insured large projects.

Insurance income of CHF 188.2 million includes interest income of CHF 17.6 million from debt rescheduling. Following the posting of loss expenses of CHF 96.9 million in the previous year, loss expenses were very high at CHF 222.3 million in 2023. SERV had to make significant provisions for losses and imminent losses in Ghana and Ethiopia. As such receivables can be rescheduled under multilateral agreements, SERV can expect to recover part of the indemnified amounts in the long term. Contrary to expectations, no significant loss expenses were incurred from insured transactions with Russia in 2023.

Premium income

in CHF million

88.1

New Commitment

in CHF bn

2.6

“Through our regional banking strategy, we want to ensure that more SMEs are informed about SERV’s support options.”

LARS pONTERLITSCHEK

Chief Insurance Officer

Marketing & acquisition

SERV focused its acquisition efforts on two topics in 2023. The first focus was the implementation of the Pathfinding Strategy. By actively marketing in buyers’ markets, it gives Swiss exporters access to major international projects, particularly those in the infrastructure sector. In collaboration with SECO, Switzerland Global Enterprise (S-GE), Swissmem, Swissrail and Suisse.ing, SERV forms part of the “Team Switzerland Infrastructure”, which jointly markets Swiss industry’s expertise in international infrastructure projects in buyers’ markets and the attractive financing opportunities opened up by SERV cover. The team’s activities during the year included accompanying Federal Councillor Parmelin on a visit to Brazil in July 2023. SERV was part of a large economic and scientific delegation led by the Federal Council.

In 2023, SERV insured three projects in Senegal, Benin and Ivory Coast via its Pathfinding Strategy, as a result of which, more than 30 exporters, for the most part SMEs, were awarded subcontracts. Several new projects are already in the pipeline for 2024.

The second focus was the development of the regional banking strategy. It is well known that banks are important multipliers in the export financing ecosystem and are able to put exporters in touch with SERV. Targeted training for corporate client advisors at Swiss banks is being employed to raise awareness of SERV products among SMEs. With regard to SME acquisition, 40 new customers were acquired in the year under review, 36 of which were SMEs.

Development of applications and new exposure

SERV approved 580 new applications in 2023, of which 451 were insurance policies (IPs) and 129 insurance commitments in principle (ICPs). The value of those 580 applications is significantly down on the figures achieved in the past. In the context of the gloomy outlook for the Swiss export economy, this decline is due to a general drop in demand for SERV insurance products. New exposure fell slightly from CHF 4.730 billion to CHF 4.432 billion. As ever, the volumes of insured transactions ranged widely, between CHF 75 500 and CHF 500 million. As is customary, the majority of transactions insured by SERV were for SMEs, which received around 80 per cent of the IPs. For ICP, demand for projects in Angola was high and SERV entered into an exposure of CHF 775 million there. The trend towards increased demand for buyer credit insurance with long credit periods, which was already evident in the previous year, continued in 2023. Three-quarters of the new exposure was for credit transactions with terms of more than two years.

Liquidity products are particularly important for SMEs. These include working capital insurance and counter guarantees. The number of working capital insurance policies issued rose from 47 to 56, while the number of counter guarantees issued remained stable at 159.

COMMITMENT & NEW COMMITMENT

in CHF million, as at 31 December

COMMITMENT & NEW COMMITMENT BY REGION

in CHF million, as at 31 December

COMMITMENT & NEW COMMITMENT BY INDUSTRY

in CHF million, as at 31 December

COMMITMENT & NEW COMMITMENT BY COUNTRY*

in CHF million, as at 31 December

COMMITMENT & NEW COMMITMENT BY OECD COUNTRY RISK CATEGORY

in CHF million, as at 31 December

COMMITMENT & NEW COMMITMENT BY SIZE

in CHF million, as at 31 December

COMMITMENT & NEW COMMITMENT BY DURATION OF CREDIT PERIOD

in CHF million, as at 31 December

Exposure & commitment portfolio

SERV’s exposure amounted to CHF 9.674 billion as at 31 December 2023, CHF 500 million lower than on the previous year’s balance sheet date. The commitment on the balance sheet date was CHF 7.892 billion, which was some CHF 423 million less than on the same date the previous year. The reduction in commitment was largely attributable to the early termination of two large buyer credit insurances in Russia and Brazil. The ICP portfolio decreased by CHF 77 million compared to the previous year to CHF 1.782 billion.

As in previous years, SERV’s highest exposure by country was to Türkiye, at CHF 1.335 billion. Angola has moved up to second place in the country list by exposure, and Kazakhstan now also ranks among the top 10 countries in terms of exposure due to a major project in the railway sector. Exposure to Russia continued to decline. Since the introduction of the sanctions adopted in 2022, SERV is no longer allowed to insure any new projects in the country, with very few exceptions. The remaining commitment amounts to CHF 389 million, a reduction of CHF 258 million compared to the previous year.

Public affairs and the national environment

Since its foundation, SERV has been committed to maintaining regular exchanges with interested business and industry associations and civil society organisations (NGOs). The Federal Council’s strategic objectives also require SERV to maintain this commitment. In fulfilling its legal mandate, SERV must take due account of the concerns of external stakeholders. Based on this mandate and the additional strategic decision to increase SERV’s public visibility, SERV began a strategic dialogue with stakeholders in 2023. These include associations and partner organisations, banks and insurance companies, civil society organisations (NGOs), parliament and the federal administration – including Swiss representations abroad.

The main objective of the meetings was to inform the dialogue partners about SERV’s mandate, range of services and working methods. The interest shown by the dialogue partners in SERV and in the concerns of the export industry was gratifying and, as a result, the public affairs activities will be continued in the coming year.

SERV’s strategy and development

SERV was also well on track in the final year of the 2020–2023 strategy period and was able to achieve its objectives for the entire period. In December 2023, the Federal Council approved the new objectives for the 2024–2027 strategy period. The Federal Council again commissioned SERV to propose solutions for its development.

The gradual process of structural change, along with the crises and events that have occurred in close succession and to some extent simultaneously, have had a major impact on the export-oriented Swiss economy and have caused its needs to change. This raises the question as to what needs to be done to ensure that SERV can continue to provide the best possible support for the competitiveness of the Swiss export industry in the future. Based on studies of the situation facing the export industry, SERV’s Board of Directors commissioned an internal project group to examine whether there is a fundamental need to reform the SERV Act. Intensive preparatory work for an open revision of the law was undertaken over the course of the year, leading the SERV Board of Directors to the conclusion that the effective future development of SERV is only possible with a focused partial revision of the legal framework. SERV is in regular contact with SECO and the Federal Finance Administration (FFA) to discuss this issue.

In alignment with the Federal Council’s new strategic objectives for SERV, the current strategy was adapted with a time horizon until 2027. Particular emphasis was placed on the themes of adaptation, innovation, transparency and resilience. The strategy covers the entire spectrum of SERV’s organisational and operational activities and is reviewed and updated annually.

International environment

After years of intensive discussions, the OECD member states reached an agreement in the spring of 2023. The Arrangement on Officially Supported Export Credits (“Arrangement”) applies to credit transactions with a term of more than two years. This modernisation is considered a milestone. During the negotiations, SERV pushed for the rules to be simplified and made more flexible in order to better accommodate the unique characteristics of individual transactions. This extra flexibility, together with the expansion of the Climate Change Sector Understanding (“CCSU”) will allow a greater number of climate-friendly projects to benefit from the more flexible conditions.

This year’s General Meetings of the Berne Union focused, among other matters, on the challenges posed by the rapidly changing geopolitical situation. In this context, the measures and adjustments adopted by export credit insurers (ECAs) with regard to their mandates and product ranges were also discussed. The transition in the energy sector and its impact on the business of ECAs was another focus area, as was the reconstruction of Ukraine and the potential role of ECAs in that process. The Berne Union is an important network for SERV, as it provides an opportunity to engage in regular dialogue with non-OECD and private export credit agencies.

SERV also cultivated its bilateral relations in the year under review. In addition to the annual, close exchange with the so-called DACH countries (Germany, Austria and Switzerland), SERV also initiated new collaborations with other ECAs, particularly in the area of reinsurance.

OECD country risk categories

As at 31 December 2023

Losses and claims

In the year under review, SERV made indemnity payments totalling CHF 53.6 million. Most of these losses were small in size. In addition, there were a number of medium-sized losses and several larger losses, including two in Ghana, one in El Salvador and one in Tanzania, as well as imminent losses in Ethiopia, which explain the exceptionally high loss expenses of around CHF 222 million.

The two losses in Ghana arose from the country’s insolvency in December 2022. The African country has halted many large projects. Many poorer countries are struggling to meet their payment obligations, in part due to the sharp rise in foreign currency interest rates in USD and EUR.

LOSSES

+24

INDEMNITY PAYMENTS

in CHF million

53.6

Some losses were averted through prompt, active pre-loss management using measures such as restructuring due dates and extending cover. Since 2020, several crises such as the COVID-19 pandemic, the conflict in Ukraine and the current conflict in the Middle East have arisen, leading to increasing uncertainty and suggesting that further losses are to be expected in the near future. Where necessary, SERV has set aside financial reserves for this purpose. To date, however, no wave of losses from the multiple crises has materialised.

In recovery, 224 losses in a total of 39 countries were processed. Recovery is often a challenging, protracted process that depends to a great extent on the country and on the debtor’s willingness or ability to pay. Initiation of legal action in the debtor country concerned does, however, give rise to some successes. Support from political actors such as embassies can also have a very positive effect on recovery in individual cases. The largest recoveries in the year under review came from India (CHF 13.8 million), the United Arab Emirates (CHF 5.8 million), Congo-Brazzaville (CHF 2.1 million) and Algeria (CHF 1.7 million). Recoveries from Bangladesh totalled CHF 1.5 million.

OVERVIEW OF LOSSES AND CLAIMS

in CHF million

Restructuring & debt rescheduling

The international agreement on a Debt Service Suspension Initiative (DSSI) for the poorest countries, reached in 2020 during the COVID-19 crisis, also impacts on the 2023 financial year: of the countries that have active debt rescheduling agreements with Switzerland, agreements under the DSSI were agreed with Pakistan and Cameroon to defer the 2020 maturities until the end of 2021. Repayments have been taking place since mid-2022.

At the end of October 2022, the Paris Club creditors, including Switzerland, managed to reach a new arrangement with Argentina on the current debt rescheduling, comprising semi-annual instalments with a repayment period of six years until September 2028. The bilateral agreement with Argentina was signed in Q1 2023. Once again, no progress was made in the negotiations with Cuba during the course of 2023.

The G20, the members of the Paris Club and other creditor countries agreed on a “Common Framework for Debt Treatments beyond the DSSI” (“Common Framework”) in November 2020. The objective of this framework is to provide countries that require support beyond that of the DSSI with debt treatment in the context of an IMF programme, with the objective of restoring the sustainability of the debtor countries’ liabilities. Chad, Ethiopia, Ghana and Zambia have submitted applications under the Common Framework. The latter three countries’ applications have implications for SERV or Switzerland. Due to the large number of different creditor groups, negotiations are dragging on. In the case of Zambia, there is an agreement in principle between the bilateral official creditors (G20, Paris Club and others) and the Zambian authorities. However, discussions with the various creditor groups are still ongoing. In the case of Ghana, discussions are also ongoing. In Ethiopia, the first step has been to agree a debt service suspension. It is also hoped that a solution will soon be found to reschedule the debt under a common framework.

SERV was impacted by the replacement of LIBOR for six countries on 31 December 2021. In the meantime, a bilateral follow-up solution has been agreed with all of the countries.

The other countries listed in the table “Credit Balances from Debt Rescheduling Agreements” with which debt rescheduling agreements were concluded in the Paris Club were able to meet their payment obligations in the year under review.

Over the course of the year, the process for assessing the top risks was refined and the compliance management system was expanded. At the end of 2023, 69.1 per cent of the Federal Council’s framework of obligation had been utilised.

Risk policy and management

In 2023, the Board of Directors (BoD) again examined in detail the risks faced by SERV and determined that risk management was appropriate. SERV is continuously developing its holistic enterprise risk management system in the interests of continuous improvement. The risk policy issued by the Board of Directors sets the framework for effective and forward-looking risk management that is in line with SERV’s legal mandate and ensures its long-term economic viability.

A variety of risk, scenario and sensitivity analyses were carried out during the year and the process for assessing the top risks was refined. The aim of this assessment is to identify and manage the main threats to net income, operational functionality, the achievement of strategic objectives or SERV’s reputation from the risk catalogue as a whole. The risk catalogue comprises strategic, financial, actuarial and operational risks, which are constantly monitored. SERV also takes into account concentration and horizontal risks, such as reputational and ESG risk, and also addresses emerging risks.

The internal control system (ICS) focuses on the identification of operational risks in key processes and on the description and implementation of suitable risk-mitigating control measures. The risks covered by the ICS are reviewed annually. The key controls are supplemented or adapted to changes in work processes as necessary.

The compliance management system, which was first developed in 2020, was further expanded to take account of the increasing requirements in this area.

On the basis of current market developments and, in particular, the business forecasts of its major clients, SERV regularly reviews its free capacities in terms of risk-bearing capital (RBC) and utilisation of the framework of obligation.

The risk policy issued by the Board of Directors sets out the framework for effective and forward-looking risk management.

Insurance obligation

The Federal Council sets out a framework of obligation that defines the maximum scope of SERV’s insurance obligations. This currently amounts to CHF 14 billion, of which 69.1 per cent had been utilised at the end of 2023.

Risks from SERV’s insurance business are assessed and handled in accordance with standardised principles. They can be hedged or minimised through reinsurance. SERV makes use of this option, for example, when country or counterparty limits are heavily utilised or concentration risks are to be reduced.

The BoD is also obliged to ensure, by informing SECO at an early stage, that the Federal Council is able to issue instructions in the case of transactions of particular significance. In 2023, four transactions underwent the process of identifying politically sensitive transactions that may be of particular significance. None of these transactions were found to be of particular significance.

Expiry of insurance obligations

in CHF million

Cover policy

SERV’s cover policy sets out the general cover principles per risk subject category (state, banks or private companies) for each country. It serves as the most important tool for risk management in the insurance business. The categorisation and the process for determining the cover status were revised in detail in 2023. To determine the cover policy, the economic, financial and political conditions of a country are analysed and the provisions of the OECD, the Berne Union and changes to the requirements contained in the legal mandate are taken into account. In addition to its own analyses, SERV also relies on external sources such as the assessments of recognised rating agencies and the OECD’s country risk categorisation (CRC). The CRC classifications are regularly reviewed and reassessed by the OECD Country Risk Experts Group. SERV is part of this group.

IN THE FIELD

Swiss Export Risk Insurance SERV supports and assists Swiss enterprises with everything from strategic direction through to the last payment for your export transaction. These three success stories tell you how.

energy_production

SUSTAINABLE ENERGY PRODUCTION SUPPORTED BY SERV

The energy transition is on everyone’s lips and sustainable energy production solutions are more in demand than ever. With its lightweight, foldable solar roofs, dhp technology AG offers a pioneering product in this field. Its business is booming, but it is impossible for the young company to cope with the risks associated with this massive growth on its own.

In view of the energy transition, the industry is called upon to find solutions for modern and sustainable energy production. One of the players offering a product that is unique on the market is the start-up company dhp technology AG (DHP). DHP has specialised in a ground-breaking product that enables the unrestricted dual use of existing infrastructure and energy generation. These are solar folding roofs which, because they are so light, can be erected over car parks or a wide range of production facilities. In addition, the folding roofs can be retracted automatically when required, e.g. in bad weather. DHP has identified a segment with great potential for its product: sewage treatment plants. They are energy-intensive and benefit from the electricity they can obtain directly on site from an installation that does not disrupt their operations.

The start-up company dhp technology makes it possible to generate energy with existing infrastructure by means of foldable solar roofs.

After DHP supplied several sewage treatment plants in Switzerland, four German operators of sewage treatment plants were also persuaded by the merits of the product in 2023. The order value of these four deliveries totals over CHF 5 million, a volume whose risks the young company cannot possibly handle alone.

“The only alternative to SERV for a young SME like ours would be expensive equity financing.”

Gian Andri Diem

CO-FOUNDER AND MANAGING DIRECTOR OF DHP

SERV, a game changer

DHP is in a start-up phase and is currently experiencing remarkable growth. With this growth comes the challenge of fulfilling large orders and managing the associated risks. The young SME is faced with a crucial dilemma: how can it scale up its operations to meet growing demand while ensuring it retains the liquidity to do so?

DHP has been able to negotiate generous advance payments for its solar panels, but these need to be guaranteed. This is where Swiss Export Risk Insurance (SERV) comes in. With its support, the risks of these advance payment guarantees could be insured and guaranteed vis-à-vis the bank. As a result, DHP does not need to deposit limits or cash with the bank and can use the advance payment effectively for the production of the export project. In addition, it is protected by SERV’s insurance in the worst-case scenario that the buyer draws on the guarantee without justification. “SERV’s insurance and guarantees are a game changer for us. The only alternative to SERV for a young SME like ours would be expensive equity financing. Those deliveries to Germany would simply not have been possible in that form,” Gian Andri Diem, co-founder and managing director of DHP explains.

The cooperation between DHP and SERV shows how innovation and ambition, coupled with the right insurance solution, can provide financial room for manoeuvre and thus give rise to remarkable success. Romeo Grass, Assistant Vice President, Large Enterprises, SMEs & Acquisition at SERV, comments: “As DHP continues to grow and contributes to the energy generation sector, its story serves as an inspiring example of the potential of innovation and collaboration in our rapidly changing world”.

swiss

SWISS SMES ARE CONTRIBUTING TO A MAJOR INFRASTRUCTURE PROJECT IN IVORY COAST

Large parts of the rural population in Ivory Coast do not have access to clean water. To tackle this problem, the Ivorian government has launched the ambitious infrastructure project “Water for all” – and Swiss small businesses are playing a big role in it. Thanks to the collaboration and pooling of expertise between various players, they are able to participate in a major project that would otherwise be out of reach for them.

Large parts of the rural population in Ivory Coast do not have access to clean water. The Ivorian government is aiming to change this with its ambitious infrastructure project “Water for all”. By delivering drinking water to people’s doorsteps in 6,000 communities, this initiative will improve the quality of life and economic situation of millions of people. Some of the supplies for the project are being sent from Switzerland. Swiss Export Risk Insurance SERV is insuring the financing of these supplies in the amount of EUR 160 million.

Access to a major international project for Swiss SMEs

The Ivorian government has chosen the general contractor Rimon CH Ltd to design and install the necessary infrastructure for about 111 communities of the communities. AquaSwiss AG, based in Frauenfeld, Thurgau, is acting as Rimon’s primary supplier and handling the logistics, engineering, materials procurement and all sub-contracted work. “For this project, we didn’t just commission well-known large corporations but SMEs as well, including a two-person workshop from Eastern Switzerland,” says Sanjeev Varma, CEO of AquaSwiss. “Without our involvement, these small businesses would not have had access to a project of this size,” he adds proudly.

The financial advisory firm Bluebird Finance & Projects Ltd has arranged the financing package for Rimon, and has structured and coordinated the whole process with SERV. Ram Shalita, CEO of Bluebird, explains why his company opted for ECA insurance from Switzerland: “This is the third time we have worked with SERV to finance a large project, so we know we can trust them. I particularly appreciate SERV’s reliability, flexibility and support when unexpected challenges arise.”

“This is the third time we have worked with SERV to finance a large project, so we know we can trust them. I particularly appreciate SERV’s reliability, flexibility and support when unexpected challenges arise.”

Ram Shalita

CEO Bluebird Finance & Projects

Patience and flexibility are also needed on this project, which according to Shalita is typical for large projects in emerging markets. SERV had been involved in the negotiations since 2019 and extended its insurance commitment in principle six times until it could eventually be converted into an insurance policy in 2023. In addition, the task of supplying 111 villages across the entire southern part of Ivory Coast is an incredible feat of logistics.

Another advantage of working with SERV is that it benefits indirectly from Switzerland’s excellent credit rating. Financing insured by SERV leads to better financing terms and can even tip the scales in an exporter’s favour when bidding for contracts.

Gil Etzion, Executive Vice President Business Development at Rimon Group, adds: “The ability to offer the Ivorian government attractive and long-term financing, on which we can rely for years until closing the deal, proved to be a tremendous advantage in winning the contract, and we definitely hope to do more large water deals in Africa with Swiss exporters and with SERV.”

satellites

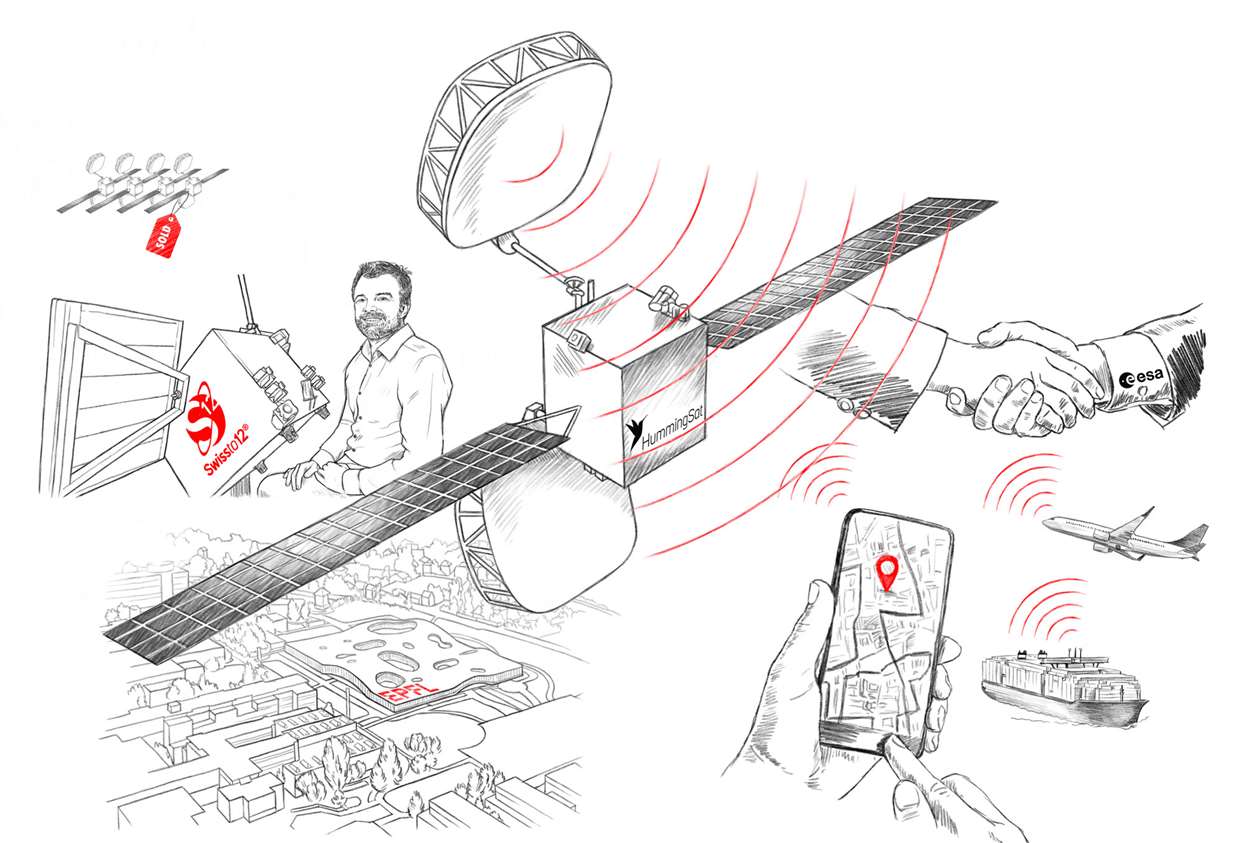

SWISS SME SHAKES UP THE SATELLITE COMMUNICATIONS MARKET

SWISSto12, an EPFL Lausanne spin-off, has become the first Swiss company to manufacture a geostationary (GEO) telecommunication satellite for commercial use. It involves a unique satellite called HummingSat, built upon SWISSto12’s patented 3D printing technology and radio frequency (RF) products. To enable SWISSto12 to supply the main players in the market, it is working with Swiss Export Risk Insurance SERV.

At around the size of an industrial washing machine, HummingSats are much smaller than conventional GEO satellites. This makes them more affordable to build, and launch costs are also reduced as they can piggyback on so-called ride-share missions. SWISSto12’s groundbreaking 3D printing technology will help boost the satellite’s performance, streamline the manufacturing process, and reduce the build time and cost of production.

Satellites must withstand harsh conditions: extreme temperatures, radiation, and intense vibrations during the launch into orbit and therefore need to use cutting-edge and thoroughly qualified technologies. SWISSto12 is not only the first Swiss company to produce a geostationary (GEO) satellite for commercial use, but with 35 patent families, the SME also has the largest worldwide patent portfolio on 3D printing technologies and products for radio frequency (RF) applications.

EPFL spin-off SWISSto12 is manufacturing a new type of telecommunications satellite using patented 3D printing technology.

When everyone pulls together

Since the company was founded in 2011, the newcomer in geostationary satellite manufacturing has raised over EUR 50 million in funding from prominent Swiss and European investors and four satellites have already been sold. In addition to that, SWISSto12 secured a CHF 25 million(EUR 26.15 million) working capital facility from UBS Switzerland AG in September. The facility, insured by SERV, will provide SWISSto12 with flexible growth capital to meet strong customer demand for its geostationary SmallSat, HummingSat.

“The insurance from SERV is enabling us to quickly fulfil orders from the biggest players in the market.”

Emile de Rijk

CEO SWISSto12

Emile de Rijk, CEO and founder of SWISSto12, explains the importance of their partnership with Swiss Export Risk Insurance: “We are shaking up the geostationary communication market, and demand is correspondingly high. The insurance from SERV is enabling us to quickly fulfil orders from the biggest players in the market.” The company currently has more than EUR 200 million in back orders from customers across its radio frequency products and subsystems business, partnership with the European Space Agency (ESA) and recent HummingSat contracts.

All parties showed a great deal of commitment and collaboration to establish this transaction. Julien Schaar, Vice President of Large Enterprises, SMEs & Acquisition at SERV, notes: “I have been impressed by the combined commitment and collaboration of Swissto12, its shareholder and its customers to getting this prestigious and ground-breaking project off the ground.”

Multi-year Comparison

As a public export credit agency that supplements private insurance products by insuring non-marketable risks, SERV’s business volume and cash flow from operations are subject to strong fluctuations. Demand for SERV insurance depends on the economic situation of the Swiss export industry, as well as on the countries in which these export transactions take place and what payment and credit terms the contracting parties agree on.

The development of new business is a calculation of the sum of all newly insured risks within one year, divided up into IPs and ICPs. Both figures are highly volatile. Years with a high volume of new business for ICPs typically alternate with years in which the volume of new business for IPs (new commitment) is high.

DEVELOPMENT OF MAIN PRODUCTS

in CHF million / number

DEVELOPMENT OF MAIN PRODUCTS – NEW COMMITMENT

in CHF million

DEVELOPMENT OF MAIN PRODUCTS

Number of policies and guarantees

If new commitments are differentiated by main products, we see that the number and volume of new commitments per product tend to be inversely proportional. For example, only a few buyer credit insurances account for a high volume of the insurances that SERV provides within a year, whereas the volume of working capital insurance and counter guarantees is spread over many different export transactions.

CASH FLOW FROM BUSINESS OPERATIONS

in CHF million

The cash flow from business operations shows whether premium payments are sufficient to finance indemnity payments and personnel and operating costs. The highly volatile nature of SERV’s business is reflected in the fact that years in which premium payments are high and indemnity payments are low alternate with years in which premium payments are low and indemnity payments are high. Total cash flow over the last 10 years has been clearly positive, i.e. payment receipts from premiums are adequate to finance payments for losses and operations.

ECONOMIC VIABILITY

in KCHF

SERV is required by law to operate in an economically viable manner, i.e. to offer its insurance services without subsidy. Economic viability represents the amount by which premium income exceeds the expected average annual loss and operating expenses per year (economic viability 1). The addition of investment income, which amounted to zero in the years up to and including 2021, results in economic viability 2. Economic viability 2 has been positive at all times over the last 10 years. As was the case last year, economic viability 2 was greater than economic viability 1 as a result of the interest income on SERV’s capital.

EMPLOYEES

Number / in %

EMPLOYEES

Number

EMPLOYEES – GENDER DISTRIBUTION

In %

The strategic objective of becoming a “trade facilitator” remains an important cornerstone for SERV’s further development. In the insurance business, the focus is on large infrastructure projects (LIP) and the implementation of the SME acquisition strategy. To this end, new positions have been created in the core business as well as in the areas of insurance and finance.

This website uses cookies to provide you with the best possible service. By using our website, you accept our data protection policy and the use of cookies.

Essentials

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Statistics

The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.