Despite the record level of CHF 89.8 million in earned premiums, SERV recorded negative net income of CHF 81.5 million due to high loss expenses of CHF 167.9 million, and thus posted a loss for only the second time in its history.

Thanks to a 19 per cent rise in new commitment and a 30 per cent increase in earned premiums, SERV was able to achieve income from insurance of CHF 91.1 million. This was offset by expenses from insurance of CHF 156.0 million due to the exceptionally high loss expenses, which led to a negative profit/loss on insurance. An increase of CHF 2.5 million for personnel and non-personnel expenses compared to 2019 and a low level of financial income resulted in an operating loss of CHF 81.5 million. As SERV is only permitted by law to invest its capital with the Swiss Confederation, it was again unable to generate income from cash investments in 2020. As a result, its net losses matched the operating loss.

Development of the Business Environment

The business environment in 2020 was dominated by the global COVID-19 pandemic and the intervention measures adopted by governments to tackle it. These measures put further pressure on the already strained fiscal situation of public finances in many countries. Ecuador and Argentina had to contend with extremely high challenges and Argentina only narrowly managed to avert national bankruptcy. In the autumn, Zambia became the first country to fall into sovereign default, in part because of the COVID-19 crisis.

The central banks of the advanced economies generally continued to pursue their expansionary stance in 2020 and, in some cases, even expanded it further. Interest rates in the emerging markets continued to be lowered. An important exception was Turkey, where, towards the end of the year, the central bank felt compelled to confront the already extended devaluation pressure on the Turkish lira by raising interest rates and thus stabilising its foreign currency reserves, which had been tight for some time.

earned premiums

in CHF million

89.8

new commitment

+19%

As an export-oriented economy, Switzerland was particularly impacted by the COVID-19 pandemic. The mechanical, electrical and metal (MEM) industries, which were already under pressure, suffered massive losses in orders and sales that they were only partly able to compensate for by the end of 2020. Mechanical engineering exports in particular only attained a level last seen 30 years ago, despite a recovery in the second half of the year. The upward pressure on the Swiss franc continued, which further weighed on the competitiveness of the Swiss export industry.

New exposure

in CHF million

Insurance policies (IP)

(new commitment)

Total

Insurance

commitments

in principle (ICP)

Total new exposure

short term

medium / long-term

2020

2019

2020

2019

2020

2019

2020

2019

2020

2019

Countries

Hungary

645.6

3.0

–

0.7

645.6

3.7

–

–

645.6

3.7

Israel

0.5

0.8

–

–

0.5

0.8

323.1

–

323.6

0.8

Turkmenistan

2.6

7.1

215.3

–

217.9

7.1

0.8

187.3

218.7

194.4

Germany

171.1

24.0

23.3

1.7

194.4

25.7

10.8

45.5

205.2

71.2

Russia

41.8

79.4

132.6

32.7

174.4

112.1

20.7

75.5

195.1

187.6

Egypt

10.0

29.5

0.6

2.5

10.6

32.0

161.1

306.0

171.7

338.0

Taiwan (Chinese Taipei)

154.6

2.9

6.7

–

161.3

2.9

–

2.2

161.3

5.1

Turkey

4.2

2.4

121.6

263.3

125.8

265.7

8.1

162.6

133.9

428.3

Other countries

463.7

810.3

585.3

912.4

1 049.0

1 722.7

697.7

625.2

1 746.7

2 347.9

Total

1 494.1

959.4

1 085.4

1 213.3

2 579.5

2 172.7

1 222.3

1 404.3

3 801.8

3 577.0

Industries

Rolling stock &

railway technology

970.9

39.4

228.8

3.0

1 199.7

42.4

4.8

96.3

1 204.5

138.7

Mechanical

engineering

194.5

413.2

294.8

317.2

489.3

730.4

464.5

833.6

953.8

1 564.0

Power generation

& distribution

9.3

45.3

226.7

542.8

236.0

588.1

398.8

187.3

634.8

775.4

Electronics

45.5

21.7

139.0

35.6

184.5

57.3

31.8

254.1

216.3

311.4

Chemicals & pharmaceuticals

188.8

340.6

–

10.5

188.8

351.1

–

–

188.8

351.1

Engineering

5.0

10.1

20.2

1.8

25.2

11.9

85.0

8.8

110.2

20.7

Metalworking

14.6

5.9

7.3

14.2

21.9

20.1

6.3

–

28.2

20.1

Other industries

65.5

83.2

168.6

288.2

234.1

371.4

231.1

24.2

465.2

395.6

Total

1 494.1

959.4

1 085.4

1 213.3

2 579.5

2 172.7

1 222.3

1 404.3

3 801.8

3 577.0

Development of New Exposure and New Commitment

After declining significantly by 46 per cent between 2018 and 2019, new commitment again increased in 2020 compared to the previous year, from CHF 2.173 billion to CHF 2.580 billion. The increase in new business volume was not, however, the result of an increase in demand for insurance from SERV. The number of new policies issued continued to decline and amounted to 576 in 2020. This compares to the previous years’ figures of 666 (2019) and 770 (2018). The growth in new exposures was primarily due to the insurance of individual high-volume transactions, which were, however, financed on payment terms of less than 24 months rather than by means of long-term export credits, which had often been the case in the past.

The decline in demand for SERV insurance reflects the huge slump in the Swiss export industry and particularly in the MEM industries as a result of the COVID-19 pandemic. New commitment continued to decline both in mechanical engineering (textile, machine tool and food processing machinery and chemical plants) as well as in power generation and distribution. In mechanical engineering, these fell from CHF 730.4 million to CHF 489.3 million, and in power generation and distribution, from CHF 588.1 million to CHF 236.0 million. Only in the rolling stock and railway technology industry did SERV record an increase in its new commitment from CHF 42.4 million to CHF 1.200 billion in 2020, which is in line with the usual volumes in previous years. New commitment in the chemicals and pharmaceuticals industries had already seen sharp falls over the last five years, and in 2020 decreased again significantly compared to the previous year, from CHF 351.1 million to CHF 188.8 million.

As SERV’s insurance of exports in the rolling stock and railway technology industry was almost exclusively on payment terms of less than 24 months, there was a demand for supplier credit insurance for these transactions. The latter has for some time seen growth in new commitment from CHF 316.1 million to CHF 864.9 million. If these rail and railway exports had been financed with a credit period of ten years or more rather than on short-term payment terms, SERV would have posted even higher premium income in 2020, despite the same level of new exposure.

Surprisingly, demand for working capital insurance and counter guarantees fell short of expectations. The number of working capital insurance policies issued fell further from 62 to 56, and the number of bond guarantees issued also declined by 4 per cent. In contrast, new commitment increased for both products, with working capital insurance seeing a significant rise from CHF 78.7 million to CHF 436.3 million. This is due to the fact that buyers were more reluctant to pre-finance their orders for individual large transactions in the infrastructure sector. SERV had assumed that SMEs in particular would be dependent on liquidity in connection with the pandemic and would therefore make greater use of counter guarantees and working capital insurance.

Overall, 58 per cent of the total new commitment was short-term in nature, i.e. insurance with a risk period of less than 24 months. This proportion is exceptionally high when compared with previous years, but does not necessarily indicate a trend.

Due to the CHF 2.580 billion in new commitment, SERV was able to achieve premium income of CHF 71.6 million. Premium income in 2020 is thus in line with the long-term average.

In contrast to the new commitment, the number of newly issued insurance commitments in principle (ICP) rose significantly from 112 in the previous year to 146. This was, however, associated with a cover volume that, at CHF 1.222 billion, was 13 per cent lower than in 2019. These changes are within the usual range for SERV. Negotiations for the export and financing of gas turbines to Israel and for a major project in Egypt’s textile sector are already at such an advanced stage that final insurance coverage can be expected in the next financial year.

SERV’s exposure came to CHF 8.971 billion as of 31 December 2020. This was slightly higher than in 2019 (CHF 8.773 billion). The commitment amounted to CHF 7.301 billion on the balance sheet date, which represented a slight increase of 3 per cent compared to the previous year’s balance sheet date.

The change in the current exposure portfolio is not solely due to the volume of new business. It is typically influenced by the writing-off of expired IP, the repayment of insured export credits, and the liability period and exchange rate changes of the insured transactions. In 2020, the COVID-19 pandemic confronted SERV with a situation in which insured transactions had to be extended much more frequently than usual due to delivery or construction delays, or the repayment period of insured claims had to be extended, often as a result of restructuring.

As in previous years, SERV’s highest commitment by country was to Turkey, at CHF 922.2 million. The country accounted for 13 per cent of total commitment. Hungary has now moved up to sixth place in the list of countries, as SERV supported a large rolling stock export transaction with working capital insurance and supplier credit insurance after the private insurance market was no longer able to provide sufficient risk capacities for this transaction.

Marketing & Acquisition

In order to mitigate the negative consequences of the government’s COVID-19 containment measures on the Swiss export industry, the Federal Council has lowered the requirements regarding the amount of Swiss content in the order value for SERV insurance and increased the maximum cover ratios for counter guarantees to 100 per cent and for working capital insurance to 95 per cent. SERV has exercised its discretion and temporarily lifted the subsidiarity restrictions for export transactions with a risk period of less than 24 months to EU member states and other high-income countries until 30 June 2021. It has done so in line with the measures of the European Commission, with which it aligns itself in accordance with the SERV Ordinance (SERV-V). In addition, SERV has simplified its checking and decision-making processes in order to make it quicker and easier for exporters to obtain an insurance offer when needed.

“SERV is an important partner for Swiss SMEs; particularly when export risks escalate.”

Heribert Knittlmayer

Chief Insurance Officer

These measures led to an increase in new customers approaching SERV in 2020, as the need for risk cover increased as a result of the COVID-19 pandemic. At 75 per cent, SMEs accounted for a very high proportion of these new customers.

The COVID-19 pandemic meant that SERV was unable to promote its 2020 ECA Pathfinding initiative as planned. In accordance with its business strategy, in the previous year SERV had already begun to increase its international profile and to identify specific projects – e.g. within the infrastructure sector – in the buyers’ markets in which Swiss exporters are able to participate thanks to SERV-insured export financing. On the one hand, projects that had been presented in Switzerland in 2019 were either put on indefinite hold or suspended completely by the buyers, while on the other, the global travel restrictions and other factors meant that almost no new projects could be identified. Nonetheless, SERV further intensified its collaboration with Switzerland Global Enterprise(S-GE) and other industry associations in order to present itself in a more coordinated manner in the buyer markets in future.

In 2020, SERV posted increased growth in new customers, with SMEs accounting for 75 per cent of this.

International Relations

In addition to the COVID-19 pandemic, international negotiations in 2020 were dominated first and foremost by the suspension of the International Working Group (IWG). Its aim was to draw up a replacement to the Arrangement on Officially Supported Export Credits (Arrangement), with the involvement of all the major exporting nations (including China and other G20 member countries). This was because not all of the countries that comprise it had previously been subject to a regulatory framework on public financing of exports, which hugely increased the risk of distortions of competition.

The failure of the negotiations within the framework of the IWG will have a major influence on the development of the only current regulatory framework for export financing, the Arrangement, which has been in force since 1978 and is affiliated to the OECD Trade Committee. It is in accordance with the principles of the World Trade Organization (WTO), which aims to prevent the official subsidising of exports. The Arrangement is legally binding in the EU countries and is adhered to in the form of a gentlemen’s agreement by all other members, including Switzerland.

The Arrangement is expected to undergo a fundamental revision in the coming years in order to reduce the complexity of its applicability and to update its current basic principles, which increasingly offer too little flexibility for current export financing practice. The EU, which, due to the legally binding nature of the arrangement, is most directly affected by the resulting competitive disadvantages, is the main driver of this modernisation process.

At the beginning of 2020, SERV commenced a two-year term as chair of the Berne Union’s ECA Committee, which is made up of all the world’s major export credit agencies (ECAs). In 2020, the regular discussions on trade and developments in the member states were accompanied by a particular focus on the measures taken in the COVID-19 crisis and the topic of sustainable development and climate change.

In addition to multilateral cooperation, SERV is constantly engaged in maintaining and expanding its bilateral relationships with other ECAs. Last year in particular, SERV benefited from this exchange and maintained an intensive dialogue with its partners in its trilateral partnership with Germany and Austria, and also with the other ECAs regarding developments in the COVID-19 crisis.

OECD country risk categories

As at 31 December 2020

Losses and claims

In addition to many smaller and medium-sized losses, SERV posted a large loss in Zambia in the year under review. The African country is heavily dependent on commodities and the fall in demand for copper in the wake of the COVID-19 crisis left Zambia insolvent to a degree.

It has so far been possible to avert many imminent losses due to the COVID-19 crisis in the year under review through prompt, active pre-loss management using measures such as restructuring due dates, extending cover and negotiating with the foreign buyers.

Losses

SERV made indemnity payments totalling CHF 82.7 million in the year under review, of which CHF 15.7 million related to payment for losses already recognised in previous years and CHF 67.0 million was newly reported losses. SERV was able to release CHF 4.6 million in provisions for imminent losses (IBNR = Incurred But Not Reported) and had to set aside CHF 111.9 million in provisions for reported losses. Value adjustments on claims changed by CHF 47.6 compared to the previous year, while SERV booked claims of CHF 11.8 million as definitive losses.

In the year under review, SERV processed 49 new losses in addition to the 176 existing losses in recovery. These new losses affected 36 countries. SERV realised CHF 11.9 million in recoveries as a result of implementing recovery measures. Of the CHF 82.7 million in disbursements for losses, CHF 26.8 million related to short-term risks in Cuba, CHF 20.3 million to risks in India and CHF 10.0 million to risks in Switzerland. The largest recovery of CHF 5.2 million and the highest write-off of unrecoverable claims of CHF 7.2 million related to a transaction in Spain. Claims from losses exceeded CHF 500 million for the very first time in 2020, rising by a total of CHF 50.1 million to CHF 501.3 million.

losses

+49

indemnity payments

in CHF million

82.7

Restructuring & Debt Rescheduling

The COVID-19 crisis has led to more than 100 countries applying to the International Monetary Fund (IMF) and the World Bank for assistance. On 14 April 2020, the official bilateral creditor countries of the G20, the Paris Club and some other creditor countries reached an international agreement on a Debt Service Suspension Initiative (DSSI) for the poorest countries. The Initiative allows these countries to use their financial resources to cover expenses related to the impact of the pandemic.

Of the countries with active debt rescheduling agreements with Switzerland, it is Cameroon, Pakistan, Honduras and Bangladesh that qualify for this DSSI. Cameroon and Pakistan have submitted a deferral request. The bilateral agreement for DSSIs with Pakistan was concluded in December 2020 (cf. Financial Report).

In October 2020, the IMF, the World Bank Group, the G20 member countries and the Paris Club agreed to extend the DSSI for another six months until mid-2021. This gave the affected countries a deferral for the repayments due in 2020 and until mid-2021, each with a one-year waiting period and a four- to five-year repayment period.

Argentina and Cuba, which do not qualify for DSSI but are nevertheless also severely affected by the impact of the COVID-19 pandemic, were also unable to meet their payment obligations in 2020. Renegotiations with these two countries are planned for the first half of 2021.

The other countries listed in the table “Credit Balances from Debt Rescheduling Agreements” (cf. Notes on the Financial Statements, p. 63) with which debt rescheduling agreements were concluded in the Paris Club met their payment obligations in the year under review.

There is currently only a purely bilateral restructuring agreement with North Korea. This expired at the end of 2019 and no follow-up arrangement has yet been agreed.

The Board of Directors (BoD) is responsible for SERV’s risk management and its monitoring. It defines the risk policy and periodically evaluates the risk profile. There were no significant changes to risk policy and risk management compared to previous years.

In 2020, the BoD again examined in detail the risks faced by SERV via regular reports. It determined that risk management was appropriate, both for the actuarial, financial, operational and strategic risks as well as reputation risks. A new compliance management system was developed in 2020 to take account of the increasing requirements in this area.

Minor improvements to risk management were defined in consultation with the Swiss Confederation based on recommendations made by Deloitte Switzerland as part of an audit of SERV’s risk capital and credit rating models conducted in the previous year. The risk capital model was extensively documented. In addition, exchange rate risks are to be taken into account in future by means of a defined factor in the risk capital.

SERV conducts an annual audit of the risks handled by the internal control system (ICS). The assessment in 2020 showed that, in terms of all the key risks, the effectiveness and efficiency of the monitoring activities were good overall. There were no significant changes compared to previous years.

On 2 July 2020, the head of the Federal Department of Economic Affairs, Education and Research (EAER), Federal Councillor Guy Parmelin, approved a new premium tariff for SERV following consultations with the Federal Department of Finance (FDF). This enters into force on 1 January 2021. The main purpose of the revision is to make the premium tariff more flexible so that SERV is able to adapt its premium regulations more rapidly.

To increase future flexibility in managing the insurance portfolio, two insurance brokers were procured through a public tender process. The brokers will be responsible for placing exposures from the portfolio on the market wherever necessary. Such sales of exposures are aimed at reducing concentration risks or employed where country limits have been heavily utilised.

The risk classification of individual countries, banks and private buyers is determined by SERV’s cover policy; it is the most important flexible risk management instrument in the insurance business. Compliance with the various limits in accordance with the risk policy, cover policy and the adequacy of the capital, and taking risk concentrations into consideration, was also reviewed in 2020 on an ongoing basis. In June 2020, the cover policy for Turkey was adjusted so that, in principle, transactions with order values of CHF 2.5 million or more with private Turkish buyers would only be insured if they were accompanied by additional bank securities. A rule was introduced in October 2020 for Argentina that, in principle, requires bank securities for all transactions with private Argentine buyers.

On the basis of current market developments and, in particular, the business forecasts of its major clients, SERV regularly reviews its free capacities in terms of risk-bearing capital (RBC) and utilisation of the framework of obligation. Of the current CHF 16 billion of the framework of obligation, 73 per cent had been utilised at the end of 2020.

In the Field

From the delivery of the largest infrastructure project in Europe, to a unique solution for the treatment of stroke patients, through to the production of high-precision data acquisition cards – three illustrative examples tell the story of projects supported by SERV in 2020.

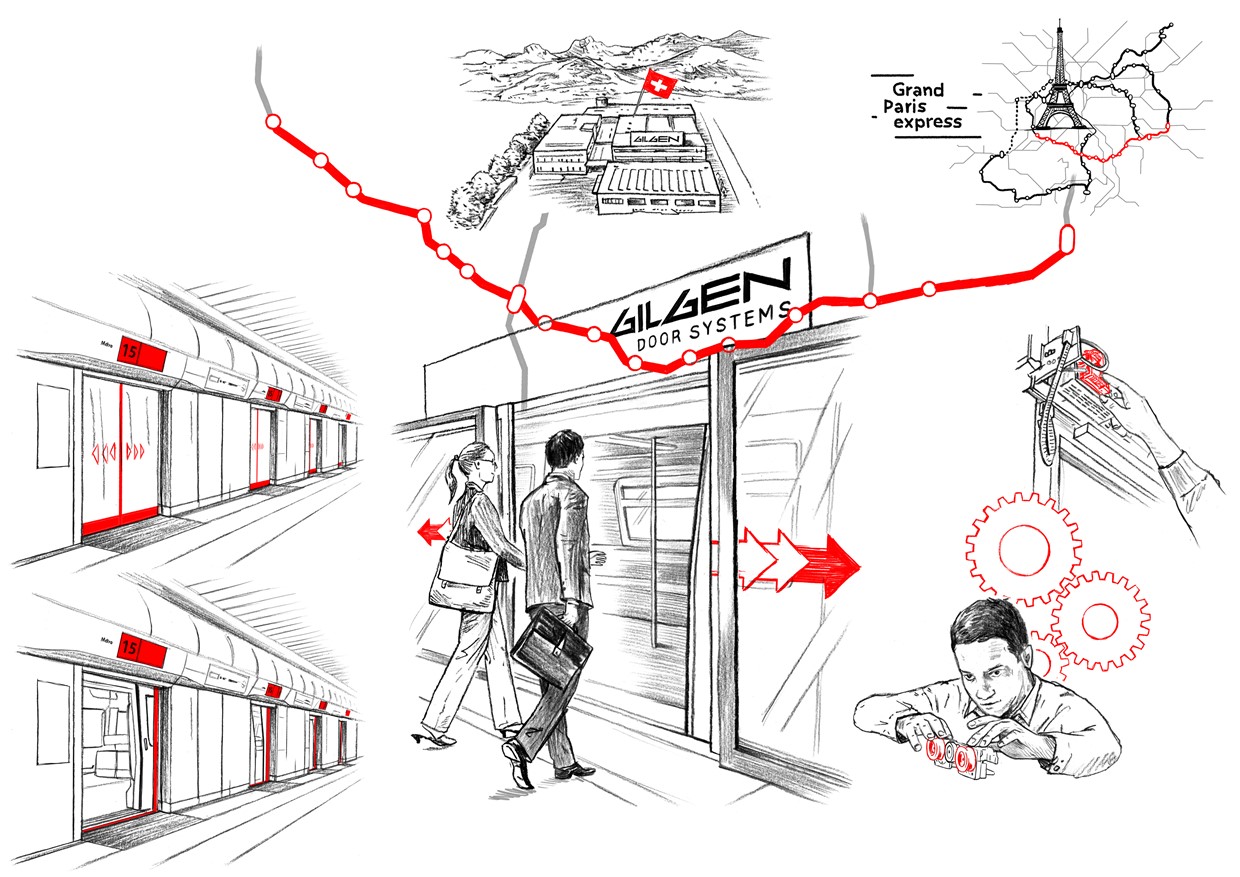

Opening the door for Gilgen Door Systems

The Société du Grand Paris asked its Swiss supplier Gilgen Door Systems AG to provide a six-figure counter guarantee for a term of more than five years. How could the Swiss exporter process this order and still keep liquidity free for other projects?

Paris is currently home to Europe’s largest infrastructure project.

Paris is currently home to Europe’s largest infrastructure project: the ‘Grand Paris Express’, operated by the Société du Grand Paris founded specifically for this purpose. As part of this project, Paris’ existing metro network is to be expanded to include a further 200 km and four additional lines. The aim is for 68 metro stations to transport around two million passengers every day by 2030.

A reliable partner

Gilgen Door Systems AG (Gilgen), based in Bern’s Schwarzenburg, was awarded the contract to work on this gigantic, prestigious project. Gilgen will be kitting out 16 stations on the ‘Line 15 South’ section with fully automatic doors, with the order value coming in at 42 million euros.

This medium-sized company has more than 60 years of experience in drive and control technology for automatic door and gate systems. When applying for tenders, Gilgen’s reputation as a reliable, competent partner offering high-quality products and services stands the company in good stead. Ultimately, this helped Gilgen win the contract. The decisive factor was its top-notch score in terms of technology and price, says Robert Hug, deputy head of ADP (Automatic Doors for Public Transport).

“We do indeed have enough liquidity, but this means that a large part of it is tied up for the entire term, so we can’t use it for other orders.”

Robert Hug

deputy head of ADP, Gilgen Door Systems AG

The buyer calls the shots

While being awarded the contract is an occasion to celebrate, it also goes hand-in-hand with major challenges: Gilgen needs to comply with an array of highly standardised requirements, all while adhering to a tight time frame. After all, “if a system doesn’t work within a project like this, it’s catastrophic. All you need is a one tiny defect and the entire metro network is brought to a standstill,” says Hug, speaking from years of experience. As a result, the French buyer requested a performance bond amounting to EUR 2.1 million, with a term of 65 months. Gilgen will be paid in instalments, in line with its progress. This means that the last payment will be made in 65 months’ time. In international tenders like this one, the negotiating margin is almost zero. Gilgen does indeed have enough liquidity, “but this means that a large part of it is tied up for the entire term, so we can’t use it for other orders,” Hug explains.

To avoid running low on liquidity, Gilgen applied to SERV for a counter guarantee, combined with contract bond insurance. This sees SERV take on the exporter’s payment risk vis-à-vis the financing bank, leaving Gilgen’s credit limits unaffected. An additional advantage is that the existing guarantee limits for its other ongoing tasks are available in full, meaning Gilgen has more flexibility in terms of pre-financing its business. In short, SERV’s support has opened the door for Gilgen to take on its next large project.

Export Risk Insurance – a Game Changer

MindMaze, a neurotechnology company based in Lausanne, offers a unique solution based on cutting edge neuroscience for the recovery of stroke patients. The demand in the market is high. But for buyers or sellers with tight liquidity, the purchase of equipment poses a great challenge. An insurance offering from Swiss Export Risk Insurance SERV can solve this problem by helping MindMaze offer competitive payment conditions and therefore triggering great sales volumes.

The neurotechnology company MindMaze is a leader in rehabilitation following brain injuries.

It is well known: a brain is damaged after a stroke. But that is not all. A less known fact is that it shows an increased ability to learn. This mechanism is called hyper-plasticity, which is highly beneficial to a stroke patient’s recovery. However, as time goes by, plasticity decreases limiting rehabilitation to a critical time window.

More than just a game

This is where MindMaze comes in: founded in 2012, MindMaze is a global leader in brain rehabilitation, with a focus on stroke patients, based in Lausanne (Switzerland). “While there are many solutions for brain recovery, MindMaze is the only company that provides an engaging solution tackling objective assessment, personalised cognitive and motor recovery simultaneously and over the full continuum of care to maximise the potential rehabilitation during and after the critical recovery phase,” Jean-Marc Wismer, Chief Operating Officer at MindMaze, says.

Based on cutting edge neuroscience, MindMaze has developed a game-based therapy called MindMotion. Created to promote the kind of movements a patient would typically practice with a physiotherapist, MindMotion is completely customisable to each patient’s needs and progress. Furthermore, the tele-health capability enables it to be used in clinics or at home. The latter allows the patient to train with more frequency and engagement while reducing the time invested by the therapist and therefore reducing the cost of treatment. Jean-Marc Wismer highlights: “Especially in times of the COVID-19 pandemic, this option is highly beneficial.”

“Without SERV’s support, we wouldn’t have been able to sign a deal of this magnitude, especially during trying economic times.”

Jean-Marc Wismer

Chief Operating Officer, Mindmaze

An enabler of growth

After extensive research, CE marking and FDA approval and pre-commercialization in 2016, MindMotion was fully commercialized in 2020. Convinced of the benefits of this product, a distributor in India ordered thousands of MindMotion licences. To enable the buyer to order a larger volume, MindMaze offered a differed payment plan with a long credit period. However, as a young company, MindMaze has limited access to credit lines or to liquidity reserves to take on such payment terms and hence ensure sales growth. This is why MindMaze asked SERV for support, and the company was able to address this challenge efficiently.

SERV covered the transaction with a supplier credit insurance. This product consists of assigning the claim and the SERV insurance to a bank which then partners with MindMaze. For its part, the bank agrees to finance MindMaze upfront against future payments to be made by the buyer “SERV enables growth companes like MindMaze for rapid commercialisation. Without SERV’s support, we wouldn’t have been able to sign a deal of this magnitude, especially during trying economic times,”Jean-Marc Wismer says.

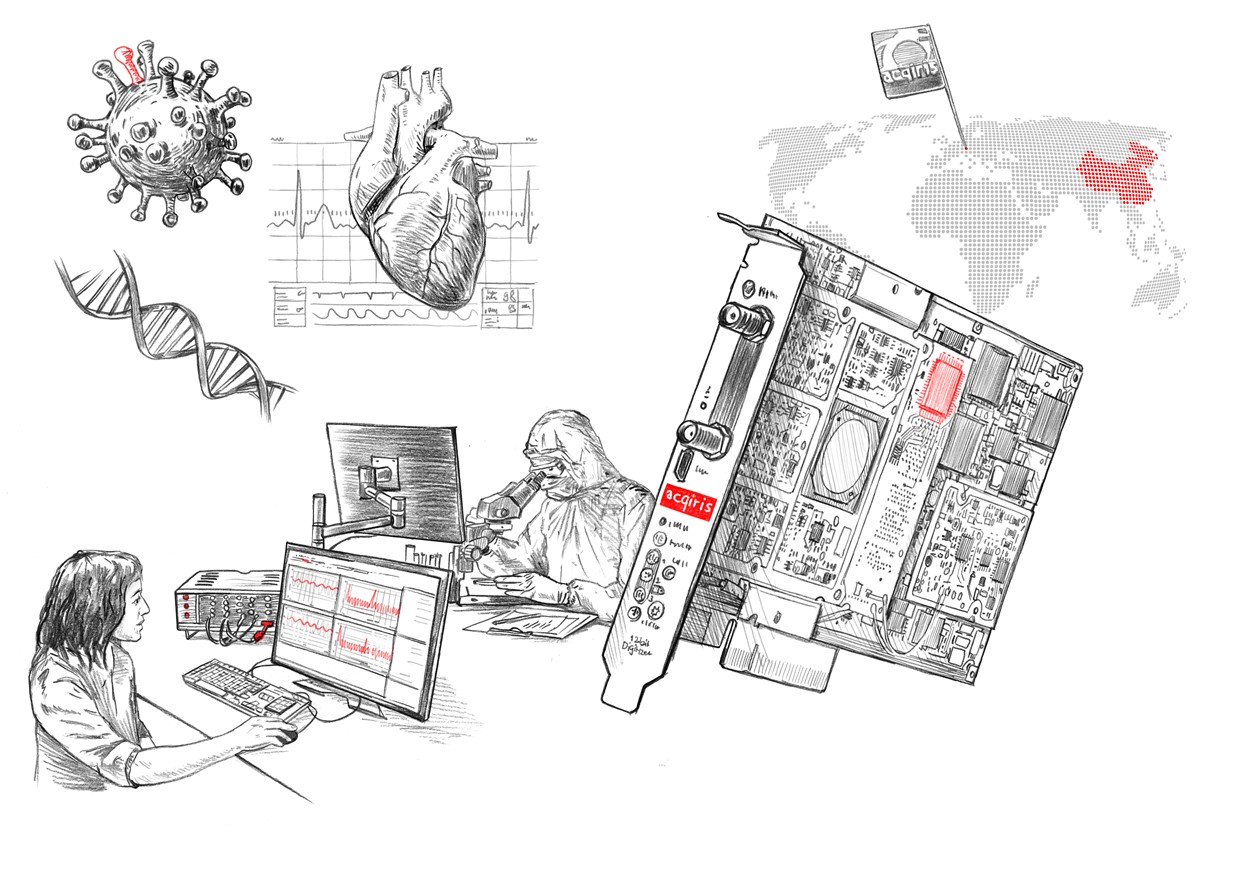

Financing thanks to working capital insurance

An SME based in western Switzerland received multiple export orders worth millions. But when it came to financing production, the company was left facing major challenges. An insurance policy from SERV gave them a helping hand.

The data acquisition cards are used in all kinds of fields.

Geneva’s suburb of Plan-les-Ouates, renowned for its watchmaking industry, is home to a small business called Acqiris. Acqiris’ data acquisition cards are even more precise than the watches made here: they accurately turn analogue signals into digital data in a billionth of a second. The data acquisition cards are used in all kinds of fields. As components within measuring instruments, they help create digital images in the sub-millimetre range, whether for treating heart disease or fighting coronavirus.

The crux of being awarded a loan

Chinese developers of high-tech medical products also use Acqiris’ cards and have placed orders totalling millions with this SME. As part of these orders, the parties agreed on one delivery per quarter, for several years. The purchaser pays for each delivery, without making an advance payment. This means that Acqiris needs to pre-finance its production costs – and here lies the crux of the matter.

Banks adhere to strict criteria when it comes to giving out loans, and Acqiris does not meet these criteria due to its unconventional history. While this SME, based in western Switzerland, was founded as far back as 1998 and has 22 employees, it was later bought by a multinational firm. It became an independent company once again in 2017 following a restructuring, which is why, officially, it is classed as a young company. “Our new form meant that our company was not old enough and did not have the necessary balance sheets to receive a traditional bank loan,” explains Didier Lavanchy, Acqiris’ co-founder.

Problem solved!

SERV was able to solve this problem: it took on Acqiris’ default risk vis-à-vis the bank via working capital insurance. In turn, the bank issued a loan that enabled Acqiris to pre-finance its production without needing to rely on an advance payment. Pre-shipment risk insurance also protects Acqiris from losses in the event that it needs to stop production through no fault of its own. “Alongside taking on the default risk, SERV’s valuable expertise helped us cover the export risks, which we are delighted about,” adds Didier Lavanchy.

“Alongside taking on the default risk, SERV’s valuable expertise helped us cover the export risks, which we are delighted about.”

Didier Lavanchy

Co-founder, Acqiris

Multi-year Comparison

As a public export credit agency (ECA) that supplements private insurance products by insuring non-marketable risks, SERV’s business volume and cash flow from operations are subject to strong fluctuations. Demand for SERV insurance depends on the economic situation of the Swiss export industry, as well as on the countries in which these export transactions take place and what payment and credit terms the contracting parties agree on.

DEVELOPMENT OF EXPOSURE PORTFOLIO

in CHF million

DEVELOPMENT OF NEW BUSINESS

in CHF million

DEVELOPMENT OF MAIN PRODUCTS

in CHF million / number

DEVELOPMENT OF MAIN PRODUCTS – new commitment

in CHF million

DEVELOPMENT OF MAIN PRODUCTS

Number of policies and guarantees

CASH FLOW FROM business operations

in CHF million

Economic Viability

in KCHF

With an exposure portfolio of CHF 8.971 billion as of the 2020 balance sheet date, the slight upward trend of the last four years has continued. Current commitments, which stood at CHF 7.301 billion at the end of 2020, have also experienced a weak upward trend in previous years. Current commitments were subject to less volatility than the exposure portfolio, which is due to the fact that SERV recorded a sharp rise in the volume of insurance commitments in principle (ICP) between 2012 and 2016, and this overcompensated for the comparatively low level of current commitments. It should be noted that SERV changed the method for calculating commitment and exposure in 2018 (cf. Annual Report 2018). As a result of the new calculation method, both figures are slightly lower than those calculated according to the previous method.

The change in the calculation method also affects new commitment (IP) as well as the new ICP issued within a financial year. Over the last four years, the volume of newly issued ICP reached a level comparable to that at the beginning of the period under review. In 2015 and 2016, on the other hand, the volume of ICP was unusually high and exceeded that of the newly issued IP. This was because SERV supported offers for a few large transactions, some of which did not materialise at all or only became orders at a later stage. As a result, SERV’s new commitment volume is in principle subject to strong volatility. For example, 2014 and 2018 were record years for SERV in terms of newly issued IP. In recent years, however, the volume of new commitment has returned to a level that is somewhat below average.

Looking at new commitment differentiated by SERV’s main products, we see that the number of newly issued supplier credit insurance and buyer credit insurance policies has tended to hover at around the same level and has even decreased slightly in the last three years. The overall increase in newly issued policies up to 2018 was therefore due to the increasing demand for counter guarantees and working capital insurance, but the new commitment volume for these nonetheless remained at a lower level compared to the other two products.

The cash flow from business operations shows whether premium payments are sufficient to finance indemnity payments and personnel and operating costs. It should be noted that, over the course of the last ten years, SERV has suffered a cash outflow from business operations in a few financial years but benefited from a substantial cash inflow in others. In total, the cash flow has been clearly positive over the last ten years, i.e. payment receipts from premiums are adequate to finance payments for losses and operations.

Economic viability 2 was also positive at all times. The surplus cover amounted to CHF 34.0 million in 2020, which was again higher than in the previous year and at a level comparable to the high values of ten years ago. Since SERV receives no income from cash investments, economic viability 2 has coincided with economic viability 1 since 2017.

Since its formation, SERV has been in a position to implement its statutory development objectives and meet its financial targets in terms of economic viability. By international standards, SERV is a highly efficient, flexible, client-oriented export credit agency (ECA). If SERV is to continue meeting both the needs of the Swiss export industry and the financial expectations of the legislator, it must be able to adapt to changes in environmental conditions and other factors by further developing its product range and making the content requirements more flexible, for example, as well as by adopting an independent investment strategy.

This website uses cookies to provide you with the best possible service. By using our website, you accept our data protection policy and the use of cookies.

)