Following the previous year’s loss of CHF 81.5 million, SERV recorded a profit of CHF 88.1 million in the 2021 financial year. In addition to earned premiums of CHF 79.4 million, the unusually negative loss expenses (income) of CHF 5.9 million also contributed to the pleasing annual result.

Although new commitment amounted to only CHF 1.933 billion, 25 per cent less than in the previous year, SERV posted premium income of CHF 83.5 million. Premiums were driven primarily by just one large transaction, in which SERV provided the Swedish export credit agency (ECA) EKN with reinsurance for the Swiss share of the project. The insurance income of CHF 90.0 million also includes interest income from debt rescheduling of CHF 10.9 million. After posting exceptionally high loss expenses in the previous year, SERV was able to release some provisions for imminent losses in 2021 and recorded successes in recovery. This resulted in negative loss expenses (income) of CHF 5.9 million. The principle of prudence in the accounting of business transactions was apparent in this regard. Some of the imminent losses reported in the previous year led to high loss expenses in 2020 and could be averted in 2021. At CHF 11.7 million, the debt rescheduling income was in line with the figure for the previous year. Personnel and non-personnel expenses rose by CHF 4.6 million compared to 2020, while financial income was positive at CHF 0.5 million compared to the previous year. In total, this resulted in an operating profit of CHF 88.1 million. As SERV is only permitted by law to invest its capital with the Swiss Confederation, it was again unable to generate income from cash investments in 2021. As a result, its net profit matched the operating profit.

SERV’s Measures to Support its Clients

The impact of the COVID-19 pandemic and its sometimes unexpected effects, such as supply bottlenecks for primary products and problems with international logistics, was a continuing theme in 2021. To take account of this challenging business environment, SERV maintained the simplifications it had created in the previous year for its clients and created new ones. The measures to support exporters during the COVID-19 pandemic that were approved by the Federal Council in 2020 remain in place. In addition, SERV introduced a fast-track risk analysis process to speed up the processing of smaller transactions.

Premium income

in CHF million

84

new commitment

–25%

“I’m pleased that our Pathfinding Initiative is beginning to bear fruit and I’m confident that the initiative will result in us insuring more large-scale projects in the future. Swiss SMEs benefit by participating in such projects.”

Lars Ponterlitschek

Chief Insurance Officer

Marketing & Acquisition

Despite the COVID-19 pandemic, SERV continued to pursue its Pathfinding Initiative vigorously. By actively marketing in buyers’ markets, it gives Swiss exporters access to major international projects at an early stage, particularly those in the infrastructure sector. The Pathfinding Initiative is the perfect accompaniment to the initiative launched by the Federal Council at the end of 2019 to give Swiss companies better access to major foreign projects. In 2021, the collaboration in Team Switzerland, which consists of SECO, Switzerland Global Enterprise (S-GE), Swissmem, Swissrail and SERV, was further expanded and also confirmed by a memorandum of understanding and advertised through a variety of measures.

SERV has already concluded an insurance transaction as a result of the Pathfinding Initiative. This involves the renewal and extension of a railway line in Ghana (cf. In the Field, 100 kilometres of railway in Ghana with Swiss participation). Several other projects are also in the pipeline. Seven foreign general contractors have opened an office in Switzerland and are in contact with over 60 Swiss companies. SERV will expand its acquisition team by two positions in 2022 and step up this initiative.

New exposure

in CHF million

Insurance policies (IP)

(new commitment)

Total

Insurance

commitments

in principle (ICP)

Total new exposure

short term

medium / long-term

2021

2020

2021

2020

2021

2020

2021

2020

2021

2020

Countries

Turkey

6.5

4.2

49.2

121.6

55.7

125.8

592.1

8.1

647.8

133.9

Russia

320.4

41.8

2.8

132.6

323.2

174.4

111.9

20.7

435.1

195.1

Ghana

0.3

0.8

264.3

–

264.6

0.8

156.2

–

420.8

0.8

Kazakhstan

0.5

0.1

–

–

0.5

0.1

343.5

–

344.0

0.1

Luxembourg

–

–

–

–

–

–

306.1

1.1

306.1

1.1

Uzbekistan

–

–

88.5

59.1

88.5

59.1

207.7

43.6

296.2

102.7

Egypt

28.0

10.0

0.8

0.6

28.8

10.6

250.8

161.1

279.6

171.7

United Arab

Emirates

184.3

18.2

8.6

17.2

192.9

35.4

85.6

19.1

278.5

54.5

Other countries

565.8

1 419.0

412.7

754.3

978.5

2 173.3

660.1

968.6

1 638.6

3 141.9

Total

1 105.8

1 494.1

826.9

1 085.4

1 932.7

2 579.5

2 714.0

1 222.3

4 646.7

3 801.8

Industries

Mechanical

engineering

290.6

194.5

337.5

294.8

628.1

489.3

777.0

464.5

1 405.1

953.8

Rolling stock &

railway technology

27.7

970.9

139.2

228.8

166.9

1 199.7

493.3

4.8

660.2

1 204.5

Engineering

96.5

5.0

3.3

20.2

99.8

25.2

84.0

85.0

183.8

110.2

Chemicals & pharmaceuticals

176.8

188.8

1.4

–

178.2

188.8

–

–

178.2

188.8

Power generation

& distribution

6.1

9.3

48.0

226.7

54.1

236.0

67.8

398.8

121.9

634.8

Electronics

11.4

45.5

3.1

139.0

14.5

184.5

18.2

31.8

32.7

216.3

Metalworking

20.8

14.6

9.0

7.3

29.8

21.9

0.5

6.3

30.3

28.2

Other industries

475.9

65.5

285.4

168.6

761.3

234.1

1 273.2

231.1

2 034.5

465.2

Total

1 105.8

1 494.1

826.9

1 085.4

1 932.7

2 579.5

2 714.0

1 222.3

4 646.7

3 801.8

Development of New Exposure and New Commitment

SERV approved 721 new applications in 2021, of which 568 were insurance policies (IPs) and 153 insurance commitments in principle (ICPs). New commitments fell by 25 per cent to CHF 1.933 billion. The volumes of insured transactions ranged widely, from CHF 19 000 to CHF 264.3 million. The majority of newly acquired insurance policies were small in volume (median of CHF 0.6 million). Almost 78 per cent of clients in 2021 were SMEs. The five largest individual commitments account for almost 40 per cent of the total new commitment. As in previous years, new commitments were predominately short-term in 2021.

Since 2017, the demand for working capital insurance (WCI) and counter guarantees (CGs) has declined continuously in terms of both numbers and exposure. The number of WCIs issued decreased further from 56 to 39 in 2021, with a fall in volume from CHF 436.3 to CHF 347.8 million. There was also a decline in the number of CGs issued, with these falling from 168 to 143. Their volume amounted to only CHF 120.8 million, some CHF 177.3 million less than in the previous year. The assumption had been that SMEs in particular would be dependent on liquidity in connection with the pandemic and would therefore make greater use of CGs and WCIs, which has turned out not to be the case since 2020.

Demand for ICPs followed a completely different trajectory: a year-on-year increase of 122 per cent to CHF 2.714 billion, with the transactions examined and accepted in principle including some large projects in the infrastructure sector with long credit periods, some of which resulted from SERV’s Pathfinding Initiative. SERV issued six ICPs, each worth hundreds of millions. This development allows us to conclude that SERV’s clients are again seeing a greater number of incoming orders following the temporary collapse in Swiss exports in connection with the COVID-19 pandemic, particularly in the machinery, electrical and metal industry (MEM industry). SERV’s business pipeline is well filled for the coming year, with the rail vehicles and railway infrastructure, power generation and textile machinery industry sectors featuring in particular. Multi-buyer insurance for the pharmaceutical industry declined further to CHF 178.2 million.

SERV’s exposure amounted to CHF 9.924 billion as at 31 December 2021, almost CHF 1 billion higher than on the previous year’s balance sheet date. The commitment on the balance sheet date was CHF 7.089 billion, which was some CHF 200 million less than on the same date the previous year. The increase in exposure resulted from the new ICPs.

The change in the current exposure portfolio is not solely due to the volume of new business. It is typically influenced by the writing-off of expired IPs, the repayment of insured export credits, and the liability period and exchange rate changes of the insured transactions.

As in previous years, SERV’s highest exposure by country was to Turkey, at CHF 1.327 billion. Ghana has moved up to sixth place in the country list as SERV has reinsured the Swiss share for a major infrastructure project for the Swedish ECA, EKN. Uzbekistan has climbed to fifth place in the country list because SERV has insured some new projects there, primarily in the textile sector.

International Relations

International negotiations on government support for export credits were dominated by the COVID-19 pandemic and climate issues in 2021, the latter of which acquired added momentum as a result of the UN Climate Change Conference (COP26) in November 2021. For example, it was agreed that, as a matter of principle, no new coal-fired power plants may be supported under the “Arrangement on Officially Supported Export Credits” (the “Arrangement”). SERV has never insured coal-fired power plants in the past and already implicitly abides by the rule now laid down in the Arrangement.

In addition to efforts to take greater account of climate targets in the Arrangement, a working group of experts has started to elaborate proposals to reform the Arrangement. The aim is to simplify the rules and increase their flexibility in order to reduce the competitive disadvantages resulting from the relatively rigid rules vis-à-vis non-OECD countries. Nonetheless, the rules must remain in line with the principles of the World Trade Organisation (WTO), which strives to prevent official subsidising of exports. SERV is actively involved in ensuring that the Arrangement is adapted to current circumstances and continues to guarantee a level playing field without generating an excessive administrative burden.

SERV has never insured coal-fired power plants in the past and already implicitly abides by the rule now laid down in the Arrangement.

SERV has chaired the committee for the ECAs of the Berne Union for the past two years. The priorities set have covered the changing role of ECAs, the impact of the COVID-19 pandemic, the climate policy and strategy of ECAs, and discussions with major export-financing international banks.

In addition to multilateral cooperation, SERV attaches great importance to maintaining and expanding its bilateral relationships. SERV maintains regular exchanges with other ECAs, including an annual trilateral meeting with Germany and Austria, which was able to be held on a face-to-face basis again in Germany in 2021.

OECD country risk categories

As at 31 December 2021

Losses and Claims

SERV reported several small and some medium-sized losses in the year under review, as well as a more significant loss in Turkey, which had, however, been on the horizon for some time. It was again able to avert some losses through prompt, active pre-loss management using measures such as restructuring due dates and extending cover. The situation has stabilised when compared to the start of the pandemic, which meant that SERV received payments made according to the normal repayment schedule in some restructured cases. SERV made indemnity payments totalling CHF 109.4 million in the year under review, including CHF 72.6 million for 28 new claims.

Claims

+28

In recovery, SERV processed 214 claims in a total of 39 countries. Depending on the country and the debtor’s willingness or ability to pay, recovery is often a challenging, protracted process. Initiation of legal action in the debtor country concerned does, however, give rise to some successes. Support from political actors such as embassies can also have a very positive effect on recovery in individual cases. The largest recoveries in the year under review came from Switzerland at CHF 4.3 million, from the United Arab Emirates at CHF 3.9 million and from Brazil at CHF 2.3 million.

Indemnity payments

in CHF million

109

Restructuring & Debt Rescheduling

The international agreement on a Debt Service Suspension Initiative (DSSI) for the poorest countries, reached in 2020 as a result of the COVID-19 crisis, also impacted on the 2021 financial year: of the countries that have active debt rescheduling agreements with Switzerland, Pakistan and Cameroon have submitted requests under the DSSI to defer the 2020 maturities until the end of 2021. Some of the bilateral agreements have already been concluded, while some deferrals under the DSSI are still pending.

Argentina and Cuba, which do not qualify for DSSI but have nonetheless also been severely affected by the impact of the COVID-19 pandemic, were also unable to meet their payment obligations in 2021, although Argentina did make a partial interest payment in mid-2021. Cuba agreed a new repayment schedule with its creditors in 2021.

The G20, the countries belonging to the Paris Club and other creditor countries agreed on a “Common Framework for debt treatment beyond the DSSI” (the “Common Framework”) in November 2020 to assist countries that require support beyond that of the DSSI to bridge their liquidity problems or whose sovereign debt is unsustainable. In the case of Ethiopia and Zambia, which have submitted an application under the Common Framework, both SERV and Switzerland are affected by their existing exposure there.

SERV is also affected by the replacement of LIBOR at the end of 2021: six countries’ debt rescheduling agreements are based on LIBOR and will need to be adjusted to a new interest rate basis. These adjustments are under way. The other countries listed in the table “Credit Balances from Debt Rescheduling Agreements (with value adjustment)” (cf. PDF Notes on the Financial Statements, p. 59) with which debt rescheduling agreements were concluded in the Paris Club were able to meet their payment obligations.

The Board of Directors (BoD) is responsible for SERV’s risk management and its monitoring. It defines the risk policy and periodically evaluates the risk profile.

Risk Policy and Management

SERV’s Board of Directors (BoD) issued updated regulations on risk policy that entered into force on 1 January 2022. The main changes concern the treatment of ratings from rating agencies, the handling of concentration risks in the portfolio, regulations on permissible foreign currencies in the insurance business and the definition of risk tolerances for foreign banks as risk subjects and for private reinsurers.

In 2021, the BoD again examined in detail the risks faced by SERV. It determined that risk management was appropriate, both for the actuarial, financial, operational and strategic risks as well as reputation risks. The compliance management system, which was first developed in 2020, will be continuously refined to take account of the increasing requirements in this area. SERV conducts an annual audit of the risks handled by the internal control system (ICS) and adapts the key controls to reflect changes in workflows as necessary.

On 31 March 2021, the Federal Council approved a revision of the insurance obligation metric based on the recommendations of an independent review of risk management. Since then, commitment (i.e. the utilisation of the framework of obligation) has corresponded to SERV’s exposure. This reduced SERV’s commitments in arithmetic terms by around CHF 2.7 billion. As a result, the Federal Council reduced SERV’s framework of obligation from CHF 16 billion to CHF 14 billion but boosted SERV’s scope for supporting Swiss exports by some CHF 700 million net. Since 2021, exchange rate risks have been taken into account in the risk capital model via a defined factor in the core capital (CCap).

By informing SECO at an early stage, the BoD is obliged to ensure that the Federal Council is able to issue instructions in the case of transactions of particular significance. In consultation with SECO, SERV implemented a new process in 2021 to identify politically sensitive transactions that may be of particular significance. In 2021, four transactions underwent this process, none of which were found to be of particular significance.

To increase future flexibility in managing the insurance portfolio, two insurance brokers were procured through a public tender process. The brokers will be responsible for placing exposures from the portfolio on the market wherever necessary. Such sales of exposures are aimed at reducing concentration risks or employed where country or counterpart limits have been heavily utilised. The insurance portfolio is analysed quarterly for concentration risks and overburdened limits in order to determine reinsurance requirements.

Cover Policy

SERV determines the risk rating of countries, banks and private buyers in its cover practice. It is the most important flexible tool for risk management in the insurance business. Compliance with the various limits in accordance with the risk policy, cover policy and the adequacy of the capital, taking risk concentrations into consideration, was also reviewed in 2021 on an ongoing basis. The cover policy for Senegal was adjusted in March 2021. Taking into account the current economic and political situation of the country and its membership of the West African Economic and Monetary Union, the insurance of banking risks was permitted in principle, as was insuring short-term transactions with private debtors. A rule was also introduced in March 2021 for Argentina that, in principle, requires letters of credit for all transactions with private Argentine buyers.

On the basis of current market developments and, in particular, the business forecasts of its major clients, SERV regularly reviews its free capacities in terms of risk-bearing capital (RBC) and utilisation of the framework of obligation. Of the current CHF 14 billion of the framework of obligation, 71 per cent had been utilised at the end of 2021.

IN THE FIELD

Swiss Export Risk Insurance SERV supports and assists Swiss enterprises with everything from strategic direction through to the last payment for your export transaction. These success stories tell you how.

100 kilometres of railway in Ghana with Swiss participation

The Swedish export credit agency EKN is collaborating with SERV, which is providing a reinsurance agreement to upgrade a railway line in Ghana. This is possible thanks to the significant involvement of several Swiss companies and benefits all parties involved in the project.

The upgrading of a 100-kilometre railway line will further boost Ghana’s economy.

Ghana is one of the fastest growing economies in Africa. In 2021, the country invested a EUR 600 million loan in the upgrading and expansion of a 100-kilometre railway line in the west of the country. This line is key to transporting goods from the inland town of Huni Valley to the port of Takoradi in the south and will further boost the country’s economy. The new rail line will initially be used mainly for freight transport, with passenger transport being gradually expanded thereafter. Known as the Ghana Western Railway Line Project, it is part of Ghana’s initiative to upgrade the infrastructure of the country’s rail network and make the line safer and faster, while simultaneously creating an environmentally friendly alternative to forms of transport that depend on fossil fuels.

A buyer credit worth EUR 523 million over a period of 18 years – including four years of construction work – is being granted for the implementation of this major international project. This is complemented by an additional EUR 75 million commercial loan for the 15 per cent down payment. Suppliers from various countries are participating in the project, including the Swiss company Molinari Rail AG (Molinari) alongside other Swiss subcontractors. Molinari offers customized solutions for the rail industry around the world. In addition, Molinari supports its clients with the design and development of vehicles as well as with project management, construction works, Q&A, commissioning, maintenance and modernization. Thanks to the considerable share of the project accounted for by Swiss suppliers, Swiss Export Risk Insurance SERV was able to provide EUR 272 million in the form of reinsurance cover.

“SERV’s reinsurance is a good way for us to participate in projects where the Swedish share is below the national content requirements by our statutes.”

Malin Tegnér Larsen

SENIOR UNDERWRITER, EKN

A set-up that benefits everyone

Amandi Investment Ltd. (Amandi), based in Cyprus, is acting as the general engineering procurement and construction (EPC) contractor, and concluded an EPC contract worth EUR 500 million with the Ghanaian buyer in mid-2020. The comparable projects that Molinari has successfully carried out in collaboration with SERV in the past enabled the company to establish a good track record. This was the factor that persuaded the general contractor to bring Molinari on board. In the words of CEO Michele Molinari, “This project allows us to demonstrate that our structure and the bundling of various subcontractors has advantages for the general contractor and is sustainable also for the ECA. For us, Ghana Railway represents a blueprint project for future contracts.”

As the largest proportion is coming from Swedish subcontractors, the Swedish export credit agency (ECA) EKN is insuring the project, but EKN’s value creation requirements do not permit it to assume the risk alone. EKN has therefore reinsured around half of the total volume with SERV. “This is a good way to participate in projects where the Swedish share is below the national content requirements by our statutes,” Malin Tegnér Larsen, senior underwriter at EKN, explains.

Although the coverage is primarily through EKN, Amandi has established a Swiss subsidiary based in Geneva called Arad Engineering SA. This is exactly in line with SERV’s Pathfinding Initiative. In the long term, this allows SERV to give SMEs the opportunity to participate in large-scale projects to which they would otherwise have no access or would struggle to access.

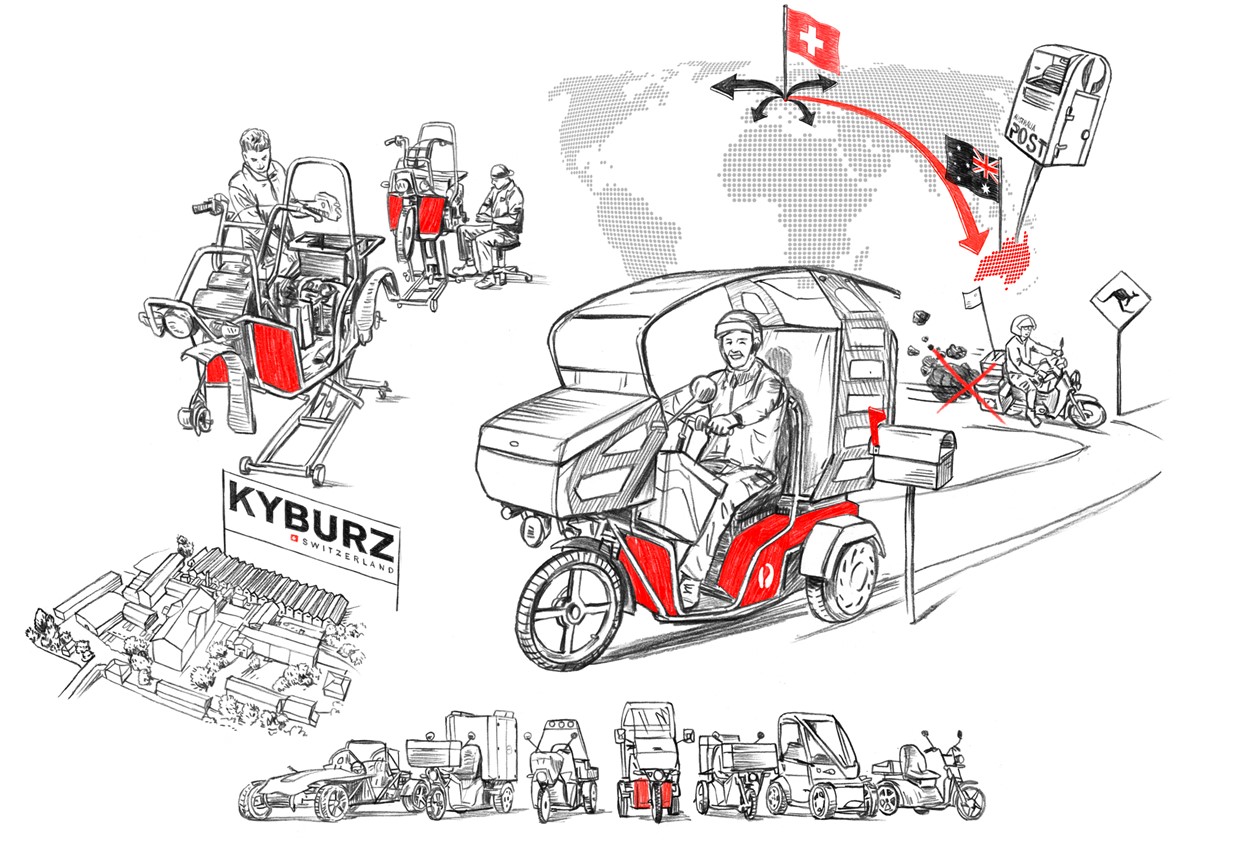

Swiss electric vehicles for Australia Post

KYBURZ Switzerland AG (Kyburz) has received a large order worth tens of millions from Australia Post and needs a loan to finance its production costs. An insurance policy from SERV is helping it to obtain lower interest rates, among other things, benefiting both Kyburz and its Australian customer.

Kyburz has received a large order worth tens of millions from Australia Post.

The company’s vehicles have been a familiar sight on Swiss streets for years. No one hears Swiss Post’s unmistakable three-wheeled electric delivery vehicles, but everyone knows them. They are manufactured by KYBURZ Switzerland AG (Kyburz), which is based in Freienstein in the Canton of Zurich. Kyburz develops and manufactures high-quality electric vehicles for delivery companies and private individuals. According to Martin Kyburz, founder and CEO of the company, “It all started in the 1980s,” when he took part in the Tour de Sol solar-powered vehicle race and discovered his passion for what were then alternative forms of propulsion. He later grew enthusiastic about developing a vehicle that was energy-efficient and fun to use, which led to the founding of Kyburz in 1991.

At Kyburz, the focus is on people and the drive to develop efficient products takes centre stage. The SME has already received several innovation awards for its developments. The company tailors its products to each individual customer’s needs, which has enabled Kyburz to attract not only Swiss Post but also a multitude of other customers all around the world. Over 25 000 Kyburz vehicles are in use worldwide. Deliveries abroad account for a large share of the company’s business.

A large order worth tens of millions

One of Kyburz’s customers is Australia Post, whose petrol-powered vehicles had seen better days. It wanted to switch to electric vehicles and chose Kyburz’s three-wheeled DXP. Following on from two large orders of 1 000 vehicles each, the company supplied another 1 000 in 2021. The Australian customer made a down payment of 30 per cent in each case against a guarantee for each of these three large deliveries, which have a combined value of approximately EUR 33 million. Kyburz receives the remaining amount only when the goods have been delivered to the customer. For an SME with more than 150 employees, that is a long time to wait for such a large sum.

The benefits of insurance

Kyburz has applied for a working capital loan from its bank to pre-finance production and ensure the necessary liquidity for other orders. SERV is insuring the loan and covering the advance payment guarantees by means of a counter guarantee. This will allow Kyburz to take advantage of lower bank interest rates and to offer the customer in Australia generous financing conditions. “The customer has high demands and attractive financing plays a significant role in being competitive,” founder and CEO Martin Kyburz explains. SERV’s support renders many financing-related questions unnecessary, allowing Kyburz to concentrate on its business and its collaboration with Australia Post.

“The customer has high demands and attractive financing plays a significant role in being competitive.”

martin kyburz

founder and CEO, kyburz switzerland AG

Martin Kyburz describes the collaboration as being based on a very high level of trust, while at the same time being demanding and intensive. The challenges are manifold, ranging from the lack of in-person contact on site due to travel restrictions, to technical problems, compliance with local legislation and cultural differences. “It puts enormous pressure on us, but also helps us to move forward,” Martin Kyburz comments. After all, we need to be ready for the next order, which will again entail fresh demands and challenges.

How an SME in French-speaking Switzerland manages to hold its own on the market

THE Machines Yvonand SA (THE Machines), which is based in French-speaking Switzerland, is doing good business. The SME is, however, confronted by the challenges of supply bottlenecks and high commodity prices and needs attractive payment terms if it is to survive in the market. SERV offers solutions to these challenges.

At THE Machines, everything revolves around pipes.

“It’s one of our best years ever,” says Jehona Gaçaferi, Export & Financing specialist at SME THE Machines Yvonand SA (THE Machines). Turnover has grown strongly over the last two years, yet, for some time now, the company has experienced new challenges, largely due to the pandemic: the SME is experiencing delays in the delivery of electronic components, and rising commodity prices are putting margins under pressure. As a Swiss company, it is also in the upper price segment. THE Machines makes up for this with its high-quality products and attractive payment terms, and it is SERV’s support that makes these payment terms possible.

Attractive payment terms thanks to export risk insurance

But what exactly is THE Machines? Everything revolves around pipes and cables at the SME. As mundane as that sounds, the solutions offered by the company, which is located near the industrial region of Yverdon-les-Bains in the French-speaking Canton of Vaud, are ingenious. It is dedicated to the development of complete, sometimes customised, production lines for the manufacture of irrigation pipes with drippers and multilayer pipes for a range of applications. THE Machines is also a pioneer in the welding of tubes in the micromillimetre range and alloys that are difficult to machine.

“We are extremely grateful for SERV’s support because we would probably have to turn down some orders if we didn’t have it.”

Jehona Gaçaferi

Export & Financing Specialist, THE Machines Yvonand SA

It has customers all over the world. They generally make only minimal down-payments and sometimes demand bank guarantees amounting to millions for the purchase of a production line. The SME, which has 60 employees, cannot handle such large orders on its own as its credit limit with the bank simply does not allow it. THE Machines has therefore relied on SERV’s insurance policies and guarantees on a regular basis for many years. “We are extremely grateful for SERV’s support because we would probably have to turn down some orders if we didn’t have it,” Jehona Gaçaferi says. SERV’s support also allows the company to enter risky markets and offer its buyers multi-year payment periods at low interest rates. It means that bank guarantees are not a problem and THE Machines’ liquidity remains intact. This collaboration has been in place since the days of the Export Risk Guarantee (ERG), SERV’s predecessor. Jehona Gaçaferi comments: “I really appreciate the relationship of trust that has developed over the years. SERV’s advisers always respond quickly and flexibly, which is indispensable for processing our transactions.”

A new strategy

Until only a few years ago, the majority of the company’s deliveries were to the agricultural sector, but there has been an increase in demand for applications for sanitary installations, heating, aviation and telecommunications in the intervening period. A high level of investment is required for the machinery for these new applications and the orders are increasingly large in volume. While this is, of course, a good thing, it necessitates adaptation to the conditions of these new markets. THE Machines has therefore introduced a new strategy. Where previously the company put stability and security first, it will in future also focus on diversification and growth. This will necessarily entail a greater need for liquidity. Jehona Gaçaferi says: “We are therefore counting on SERV’s support in this growth phase.”

Multi-year Comparison

As a public export credit agency (ECA) that supplements private insurance products by insuring non-marketable risks, SERV’s business volume and cash flow from operations are subject to strong fluctuations. Demand for SERV insurance depends on the economic situation of the Swiss export industry, as well as on the countries in which these export transactions take place and what payment and credit terms the contracting parties agree on.

The development of new business is a calculation of the sum of all newly insured risks within one year, divided up into IPs and ICPs. Both figures are highly volatile. Years with a high volume of new business for ICPs typically alternate with years in which the volume of new business for IPs (new commitment) is high.

DEVELOPMENT OF MAIN PRODUCTS

in CHF million / number

DEVELOPMENT OF MAIN PRODUCTS – NEW COMMITMENT

in CHF million

DEVELOPMENT OF MAIN PRODUCTS

Number of policies and guarantees

If new commitments are differentiated by main products, we see that the number and volume of new commitments per product tend to be inversely proportional. For example, a high volume of the insurances that SERV provides within a year are accounted for by only a few buyer credit insurances, whereas the volume of working capital insurance and counter guarantees is spread over many different export transactions.

CASH FLOW FROM BUSINESS OPERATIONS

in CHF million

The cash flow from business operations shows whether premium payments are sufficient to finance indemnity payments and personnel and operating costs. The highly volatile nature of SERV’s business is reflected in the fact that years in which premium payments are high and indemnity payments low alternate with other years in which premium payments are low but indemnity payments are high. In total, the cash flow has been clearly positive over the last ten years, i.e. payment receipts from premiums are adequate to finance payments for losses and operations.

ECONOMIC VIABILITY

in KCHF

SERV has a legal requirement to operate in an economically viable manner, i.e. to offer its insurance services without subsidy. Economic viability represents the amount by which premium income exceeds the expected average annual loss and operating expenses per year (economic viability 1). The addition of investment income, which amounted to zero in previous years, results in economic viability 2. Economic viability 2 has been positive at all times over the last 10 years.

Employees

Number / in %

EMPLOYEES

Number

EMPLOYEES – GENDER DISTRIBUTION

In %

The reasons for the steady increase in staff numbers can be explained as follows: the number of insurance applications and claims reports has risen in recent years, but the legal requirements that SERV is subject to have also increased (particularly those relating to procurement and data protection). SERV has had to increase its workforce in the last two years to cope with the renewal and expansion of its IT systems.

This website uses cookies to provide you with the best possible service. By using our website, you accept our data protection policy and the use of cookies.

)